This article was first published by Carrier Management on October 15

By Tony Buckle and John Carolin | October 15, 2024

When actual prices line up with technical prices, insurers expect underwriting profits to emerge. But what if underwriters find ways to adjust technical prices downwards? Based on interviews with underwriters conducted for their research, Tony Buckle and John Carolin, co-founders UWX, suggest that truer leading indicators of performance come from listening to the open and honest assessments of underwriters and keeping track of actions of managers.

Related Part 1 article: “Soft Commercial Market Ahead: Prepare for Underwriter ‘Herd Behavior‘”

Prices are under pressure in many insurance markets.

After an extended period where pricing levels have risen and held at profitable levels, the balance of power appears to be shifting to buyers. In segments such as management liability and cyber, this shift has been dramatic, with loss-free accounts attracting reductions of 50 percent or more year on year.

“When the herd moves, it moves,” as the former British Prime Minister Boris Johnson once ruefully said. Momentum shifts are tough to manage.

Momentum shifts, such as those seen in a softening market, are even tougher. They prompt fear and irrational actions as the following quote from our research illustrates.

“We knew terms and conditions were not good, but the competitors wrote it if we did not.”—Senior Underwriter, Global Insurer, EMEA.

To paraphrase Rudyard Kipling, how do you keep your head when all about you are losing theirs?

The key is to plan for market softening now, when insurance markets remain relatively robust, portfolios profitable and emotions in check. With cool heads, define now the actions you want to take when markets soften. It is far easier to draw red lines when profits are strong than when “under the pump” of an ambitious premium target in a plunging market.

“The key is to plan for market softening now, when insurance markets remain relatively robust, portfolios profitable and emotions in check. With cool heads, define now the actions you want to take when markets soften.”

The key to planning is knowing when to act—when to apply the brakes and also when to press the accelerator. This requires metrics that are focused on leading indicators of performance, i.e., measuring the activities today that will drive the results in the future. Lagging indicators of performance that focus on the outcomes of yesterday’s actions, such as accounting profit, come far too late for timely management intervention.

The shift to true leading indicators is not straightforward. Many carriers employ pricing outcomes as leading indicators, such as technical price adequacy, which tracks the actual price achieved in the market relative to the technical price the particular risk required. This sounds reasonable, until you assess the behavior around the calculation of technical price.

Tweaking the Tools

Behavior was the focus of the UWX research, and the study found that tools were regularly manipulated to achieve the desired outcome. Here are sample quotes from across the globe:

How objective is technical price if underwriters can manipulate the pricing tools to get to the price they need? How predictive of performance is technical price adequacy? How comparable are technical prices from different years? What does that imply about the rate adequacy and ultimate loss ratio of the portfolio as a whole?

What you really want to be measuring is pricing integrity, i.e., the behavior around pricing tool usage. How the tools are being used, or abused, is not only much more predictive of ultimate profitability but can also be assessed and addressed before the harm is done.

The UWX research showed further that there was a distinct cycle to behavior. The International Association of Engineering Insurers (IMIA) graph below shows rates for different types of engineering and construction insurance between 2002 and 2022. The shape of the graph will be familiar to underwriters in many lines of business. Rates declined steadily post the horrific terror events of Sept. 11, 2001 and hit their nadir in 2017/2018. From there, rates have recovered.

Source: Global Market Stats & Benchmarking, IMIA 2022

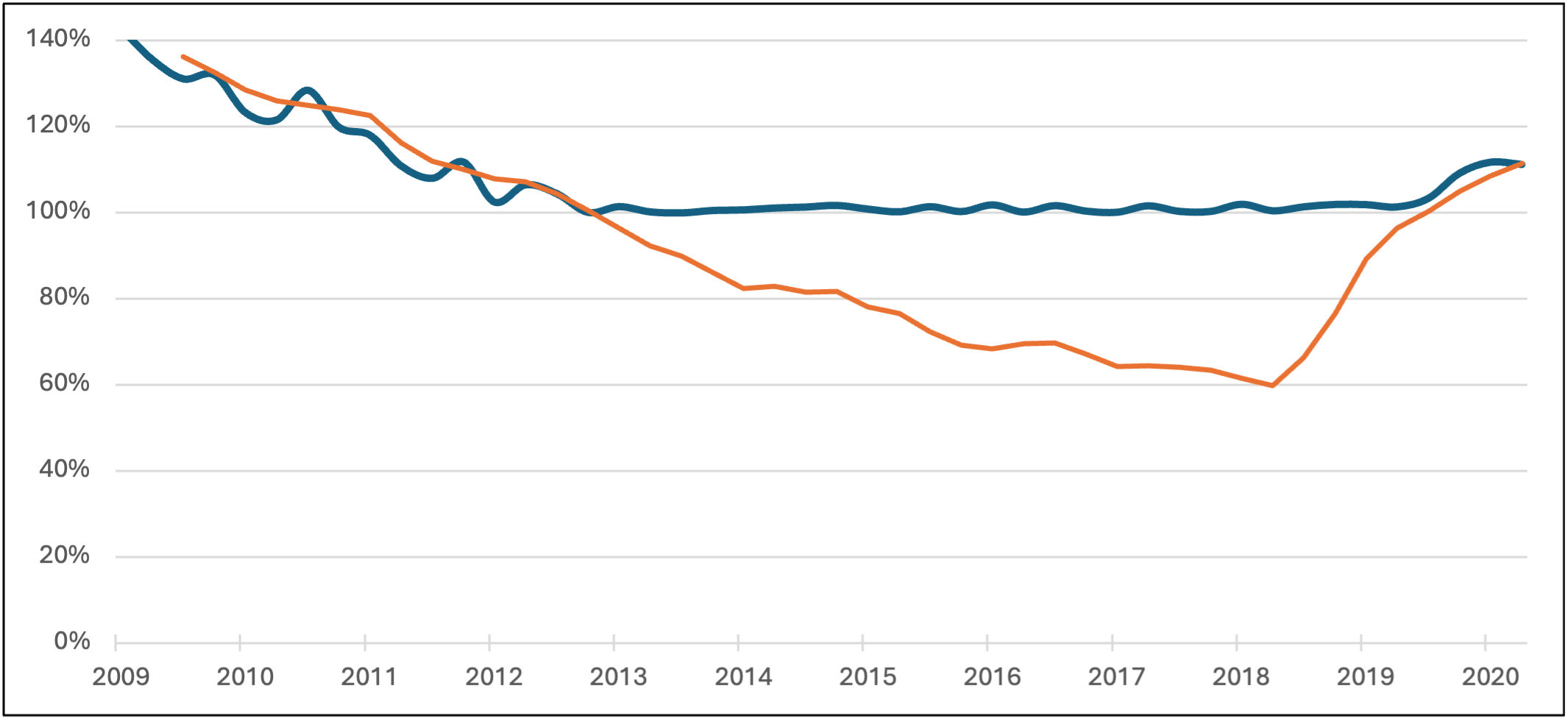

Combining the rates above into one line (shown in red in the chart below), UWX analysis overlaid the technical price adequacy of one particular engineering and construction portfolio over the same period (shown in blue below). What can be seen is that as long as price adequacy remained above 100 percent, portfolio rate adequacy essentially moved in line with overall market rates. However, once price adequacy approached 100 percent, the lines deviated.

Source: UWX, 2024

There could be multiple explanations for this. It could be that underwriters of this particular portfolio rejected any risks that priced below 100 percent technical rate adequacy. Perhaps underwriters replaced rate inadequate risks with rate adequate ones. Or perhaps underwriters found ways to adjust the technical price downwards? Whatever the cause, our point is that there is a behavior change that can be measured and investigated.

Current control systems often unwittingly exacerbate the problem. For example, insurer guidelines often impose special rules around risks that do not achieve 100 percent rate adequacy. Combine that constraint with pressure to achieve premium targets in a plunging market, and you create the perfect storm. Compromises are made.

“Being a professional underwriter during the soft market at least in my experience was really compromising on a lot. On too much. That was, at least for me, the most difficult part. Knowing you’re doing something which is in principle wrong but just executing because that’s what you are requested to do.”—Underwriting Manager, Reinsurer, EMEA.

Behavior Is Key

One objection often leveled at behavioral measures—notably around perceptions and attitudes—is that staff are unwilling to “tell is as it is.” The UWX research does not support this. While compromises were made in the soft market, where management encouraged open and honest communication, open and honest communication is what they got. The problem was much more that underwriters’ views were either not sought, were ignored or were overridden, as the following quotes demonstrate:

Underwriters and Tools

Engineering and construction is a complex insurance class, covering risks as diverse as battery storage, nuclear power plants and road tunnel construction. Tools in broad use across the segment therefore, such as PUMA (Swiss Re) and the Munich Re Engineering Tool, offer a lot of flexibility and discretion to the underwriter both in classification of the risks being underwritten and how they are assessed (contractor quality, vulnerability of location, build-up of values, etc).

All these factors drive pricing tool adjustments that impact the technical price.

Unfortunately, current feedback mechanisms like annual employee engagement surveys are next to useless in this regard. They do not provide the timely or relevant feedback on market dynamics that managers need to steer their businesses effectively. The UWX study found that underwriters were highly engaged during the period 2013–2017. At the same time, they were decidedly clear-eyed about the prevailing market reality and the pressures upon them (for example, to hit premium targets). Measuring those sentiments, rather than engagement, would have been much more predictive of performance.

Best-in-class insurers have long recognized such problems. They are recognizing how market forces can affect metrics like cost ratio, net promoter score and market share and how these can encourage unprofitable underwriting if not contextualized. Most important, they focus on measuring behaviors, not just among their own underwriters but across the market.

It would be wrong however to focus exclusively on underwriter behavior. It is vital to also measure management actions in respect of underwriting. Increasing premium targets in a softening market for example. Or more specifically, tracking the number of deals being escalated to executive level for decision-making. Such metrics provide useful insight into management discipline.